A new report, from Housing Australia, has revealed that about one in three of all first home buyers in the 2022-23 financial year used the federal government’s Housing Guarantee Scheme (HGS) and its three different assistance programs.

Here’s what the typical participant looked like, according to Housing Australia:

Housing Australia has not only taken control of the HGS, but also the National Housing Infrastructure Facility, which provides loans and grants for critical infrastructure to unlock and accelerate new housing supply.  The latest Reserve Bank of Australia (RBA) data has shown the impact the RBA's cash rate rises have had on the mortgage market. The key is to compare average interest rates for all outstanding loans in April 2022 – the month before the first rate rise – and August 2023 – the most recent month for which we have data. During that time, the RBA increased the cash rate by 4.00 percentage points. Interest rates for outstanding loans have, on average, increased by less than that amount, in part because some loans were fixed at lower rates. For owner-occupied loans, rates have increased by an average of:

For investment loans, rates have increased by:

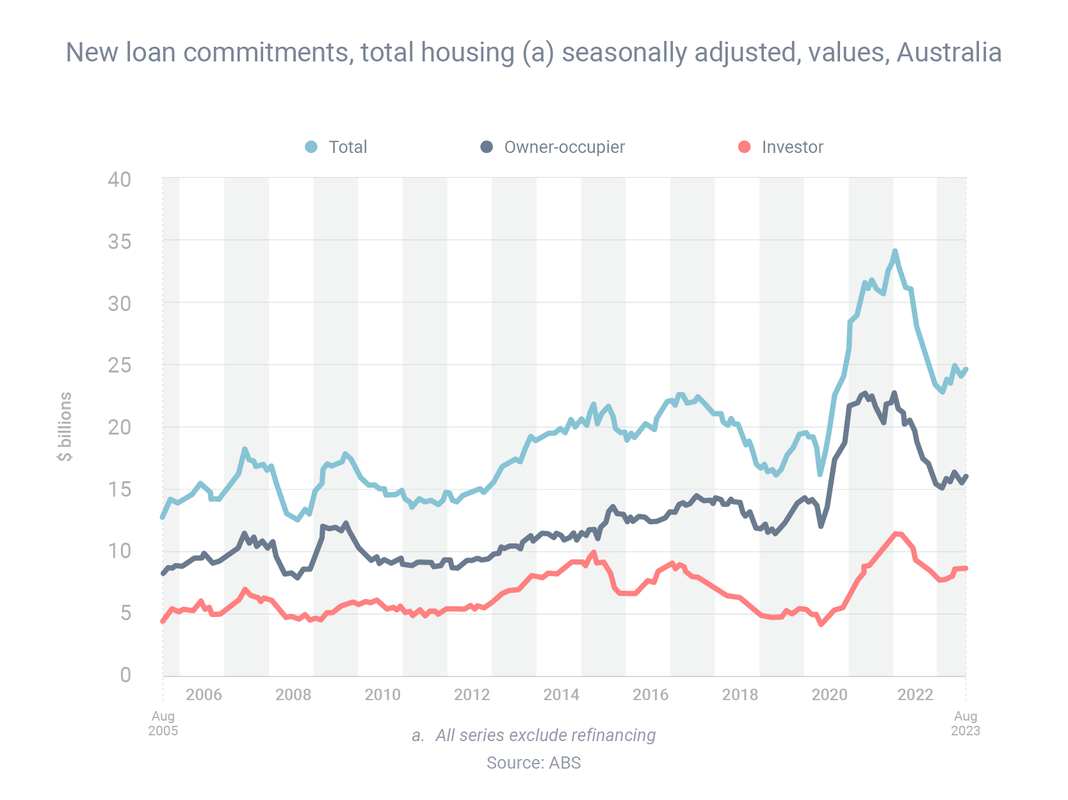

With lots of people coming off fixed rates right now, it’s no surprise that an enormous amount of refinancing is occurring, as borrowers look to switch to lower-rate loans. The latest Australian Bureau of Statistics (ABS) data has revealed that borrowers did $20.60 billion of refinancing in August – which was 3.9% lower than the month before but 12.4% higher than the year before. Meanwhile, the ABS also revealed that the value of all new home loan commitments in August was $24.82 billion, which was 2.2% higher than the month before. Owner-occupier borrowing rose 2.6% to $16.07 billion, while investor borrowing rose 1.6% to $8.75 billion. That said, home loan activity has fallen on a year-on-year basis:

The interest rate environment has changed a lot recently, and the level of competition in the mortgage market is fierce, so there are a lot of great refinancing deals available – including with quality smaller lenders you may be unfamiliar with.

Household savings have now fallen for seven consecutive quarters, suggesting some consumers are finding it harder to save for a home deposit due to rising cost of living. The latest Australian Bureau of Statistics data show that the share of income that households save fell significantly between the quarters of September 2021 and June 2023:

This decline in saving has been partly caused by the pandemic: people spent less during lockdown, because they were stuck at home, and then engaged in 'revenge spending' after being released. But it’s also been caused by the high inflation we’ve experienced during that time, which has forced consumers to spend more money just to buy the same items.

If you have a mortgage and you’re struggling to make repayments, get in touch so we can speak to your lender. Lenders tend to be more flexible with borrowers who get on the front foot about any financial problems they may be experiencing.  Interest rates influence property prices, but they are not the reason that Australia has some of the highest housing values in the world, Philip Lowe said in a speech just before standing down as Reserve Bank governor.

Mr Lowe said it's true that the lower interest rates that Australia has experienced for much of the past 30 years have contributed to the increase in property prices. "But the reason that Australia has some of the highest housing prices in the world isn’t interest rates, which have been at roughly similar levels across most advanced economies. Rather, it is the outcome of the choices we have made as a society: choices about where we live; how we design our cities, and zone and regulate urban land; how we invest in and design transport systems; and how we tax land and housing investment," he said. "In each of these areas, our society and politicians have made choices that lead to high urban land and housing costs. It is by tackling these issues that we can address the high cost of housing in Australia, which I view as a serious economic and social problem."  The federal government's Home Guarantee Scheme (HGS) is helping first home buyers on modest incomes enter the market with small deposits, according to research commissioned by the National Housing Finance and Investment Corporation.

Some of the key findings from the research were:

Under the HGS, first home buyers can enter the market with just a 5% deposit – but conditions apply. I can tell you whether you’re eligible and help you apply for a loan.  The combined value of Australian real estate reached $10 trillion at the end of August, according to CoreLogic, which is the first time it's reached this level since June 2022. The increase resulted from a combination of more properties being built and the value of Australia's housing increasing. Soon after reaching the $10 trillion mark last year, the property market began a 10-month downswing, during which the national median property price fell 9.1%. Since March, prices have risen in six consecutive months, increasing by a combined 4.9%. However, the outlook is uncertain, according to CoreLogic.  “While there is a growing expectation that the RBA board is done hiking the cash rate, borrowing remains constrained by a relatively high serviceability buffer,” CoreLogic said.

“APRA [banking regulator] data to June showed the weighted average home loan assessment rate was just below 9%, and Australian Bureau of Statistics housing lending data shows mortgage lending has fallen for three of the past four months.”  New data from CoreLogic suggests we might be near the end of the housing downturn. While Australia’s median property price fell 0.1% during February, values then rose in some markets in the four weeks to March 15:

That said, it’s too early to call the bottom of the market, according to CoreLogic’s executive research director, Tim Lawless.

“Interest rates may rise further from here, as well as the fact that we are yet to see the full impact on households from the aggressive rate hiking cycle to date,” he said. “Additionally, economic conditions are set to weaken through the middle of the year, as household savings buffers are being depleted and labour markets are likely to loosen further.” Mr Lawless said one of the key metrics to watch would be the flow of new property listings, as a relative increase in supply would lead to a relative decrease in demand, and “could be a signal this recent trend of growth has run out of steam”.  The rental market has turned decisively in favour of property investors, with the number of vacant rental properties plummeting by one-third over a 12-month period. Between January of 2022 and 2023, the number of rental vacancies across Australia fell from 47,977 to 31,592, a reduction of 34.2%, according to SQM Research.  At the same time, the vacancy rate – which measures the share of untenanted rental properties – fell from an already-low 1.6% to just 1.0%.

Vacancy rates differ from city to city, but are low throughout the country, ranging from 0.4% in Perth to 1.6% in Canberra. SQM Research managing director Louis Christopher said low vacancy rates were contributing to a “surge in rents”, which in turn was pushing up rental yields. “I believe would-be investors will be attracted to higher rental yields in later 2023, provided the cash rate peaks at below 4% [it's currently 3.35%],” he said  Despite the recent housing downturn, property prices are higher in most parts of the country than before the pandemic. As a result, deposit requirements are higher. Domain compared property prices in the December quarters of 2019 and 2022, and found that buyers needed tens of thousands of dollars more today if they wanted to buy a house and put down a 20% deposit. The increase in 20% house deposits for our four biggest cities was:

While the deposit barrier is high, it’s not insurmountable.

As an expert mortgage broker, I can potentially help you enter the market with a low-deposit loan. Generally, if your deposit is lower than 20%, you will need to pay lender’s mortgage insurance (which can be added to your loan). While it’s never nice to pay an added fee, it can be money well spent if it lets you buy a property several years ahead of schedule  Home building costs continue to rise sharply, but it appears the worst is behind us.

Residential construction costs rose 11.9% during 2022, after climbing 7.3% in 2021, according to CoreLogic’s Cordell Construction Cost Index (CCCI). The 2022 result was the largest annual increase on record, apart from the period impacted by the introduction of the GST. However, the pace of growth appears to be slowing: prices increased 4.7% in the September quarter, but only 1.9% in the December quarter. CoreLogic construction cost estimation manager John Bennett said, in 2023, costs would be unlikely to rise at the same rapid pace as in the recent past, because rising interest rates and inflation have made consumers, builders and suppliers more cautious. Analysing the price increases, Mr Bennett said:

Many property investors enjoyed a big rise in their rental income during 2022. CoreLogic has reported that the median rent for an Australia investment property increased 10.2% during the year. The city-by-city breakdown was:

"Rents are still rising in most capital cities and regional areas, with vacancy rates low," according to CoreLogic head of research Eliza Owen.

Between September 2020 (when this period of rental increases began) and December 2022, Australian rental rates increased 22.2% – the largest increase in a 27-month period in recorded history  Refinancing activity is at ultra-high levels right now, as owner-occupiers and investors alike try to find home loans with lower interest rates as the Reserve Bank continues to raise the cash rate. Borrowers refinanced a record $19.5 billion of loans in November, the most recent month for which we have data, according to the Reserve Bank of Australia. By way of comparison, that was 20.4% higher than the year before and 88.2% higher than two years before.  The Reserve Bank has hinted that at least one more rate rise is coming. In December, it said it wanted to "return inflation to the 2-3% target range over time" (it's currently 7.3%) and would “do what is necessary to achieve that outcome" – i.e. further increase the cash rate.

So if it’s been a while since you took out your home loan, now would be a good time to think about refinancing. Contact me to get the ball rolling. I’ll be happy to crunch the numbers for you, so you can see if refinancing would be suitable for you and how much money you could save by switching to a comparable lower-rate loan.  One of the world’s largest real estate firms has given five very good reasons why “Australian real estate represents a compelling investment”.

I can help you secure finance to buy a property, whether it’s to live in or for investment purposes  Home loan activity has fallen since earlier in the year, but demand among first home buyers has held up better than that of other buyer groups.

Between April, when national property prices peaked, and August, the most recent month for which we have data, total home loan commitments fell 13.9%, according to the Australian Bureau of Statistics. However, the decline varied between different buyer groups:

CoreLogic's head of residential research, Eliza Owen, who analysed downturns since 2004, found first home buyer demand for finance during downturns has traditionally been resilient, with smaller falls in demand compared to the other two groups, and sometimes even increases. Ms Owen said there were two reasons for this:

The increase in interest rates over the past six months has made it harder for Australians to qualify for a home loan, and made it more important they get help from a mortgage broker.

Every rate increase of 0.50 percentage points reduces an average borrower’s maximum loan size by about 5%, according to the Reserve Bank’s head of domestic markets, Jonathan Kearns. Since May, the Reserve Bank has increased the cash rate by 2.50 percentage points – which means the average person’s borrowing capacity has fallen by about 25%. The key words here are ‘average’ and ‘about’ – because borrowing capacity varies not just from person to person but lender to lender. Two banks can offer the same borrower very different maximum loan amounts; sometimes, they might be more than $100,000 apart. With borrowing conditions getting harder, it’s vital you seek guidance from an expert broker. I work with a large panel of lenders, so I know which lenders would be more likely to offer finance to someone with your scenario. I can then present your application in such a way as to maximise your chances of approval  New analysis has revealed two big reasons why rents, which are already rising steeply, are set to continue increasing. First, the number of properties listed for rent is much lower than pre-pandemic, in both capital cities and regional areas, according to PropTrack economist Angus Moore. So supply has fallen. Second, Australian Bureau of Statistics data show a significant increase in migrant and foreign student numbers. That means demand is rising. "Extra demand from returning migration amid tight housing availability will contribute to the ongoing rapid advertised rent price growth we are seeing," he said.   "We’re already seeing signs consistent with that dynamic. Rents are growing especially quickly in areas that recent migrants typically move to – these are mostly inner-city areas, often near major universities."

Mr Moore said "rents are likely to continue growing briskly" in the foreseeable future. "Vacancy rates are low across much of the country and, with population growth returning, rental demand shows little sign of tempering.  Monday and Tuesday this week, I had the privilege of sitting alongside some absolutely inspirational women and men of the finance industry, as part of the Mortgage and Finance Association of Australia (MFAA) Opportunities for Women's panel meeting and lunch launch, presented by key lead researcher Jane Counsel.

The initiative seeks to deliver findings, consider actions and future initiatives for the finance industry, and particularly targeting inclusion and diversity in the finance industry, particularly around that of the participation of women. Questions discussed at length, were not limited to retention of women in the sector, but also the support of, and attracting more women to finance, and understanding the challenges that women face. Notable that while industry participation overall is on the rise, female representation has decreased from 28% to 25% in recent years, and understanding why, and what can be done to counter this trend, is critical to long term success. Aside from meeting some wonderful members of the broader community, including lender, and aggregator representation at the launch, it was also a pleasure to meet AFLW player Sabrina Frederick, who shared her story and experience, as a professional AFL player, who was wonderfully inspiring and a joy to listen to. Much thanks must go to Stephen Hale, Usha Dean & Mike Felton, along with the ever insightful, supportive and inspirational Jane Counsel, along with all of the other participants who welcomed me and my contributions so warmly.  The Reserve Bank of Australia (RBA) increased the official cash rate by 25 basis points to 0.35% at today’s board meeting.

This is the first cash rate hike in more than a decade and comes after core inflation grew by 3.7% over the year to March – well above the RBA's 2-3% target. With the latest inflation data, it shows that Australia had recorded the highest quarterly and annual increase in more than two decades. The last time the RBA increased interest rates was in November 2010. The official cash rate has been at a record low of 0.1 per cent since November 2020. Mortgage holders have been warned to prepare for a double rate rise. The cash rate is largely expected to jump by 1 per cent by the end of this year and reach 1.25 per cent next year. Lenders are likely to lift mortgage rates in line with the cash rate increase, which may result in big changes to variable home loan repayments. Reach out so we can review your home loan.  Mortgage brokers were responsible for 66.5% of all new home loans in the December quarter, according to the latest data from research group Comparator. That is not only a record for a December quarter, it's also a significant increase on the market share brokers recorded in December 2020 (59.4%) and December 2019 (55.3%).  Mike Felton, the CEO of the Mortgage & Finance Association of Australia, said the strong increase in mortgage broker market share shows that consumers really value the service, competition and choice that brokers provide.

When you visit a bank for home loan advice, the bank will only tell you about its own products, even if it knows another lender is offering a better home loan. But when you visit a broker, the broker will compare interest rates, loan features and borrowing criteria from a range of lenders. The broker will also negotiate with lenders on your behalf. That significantly increases your chances of getting a great loan that’s tailored to your unique circumstances.  When it comes to classifying debt as either ‘good’ or ‘bad’, borrowing to fund your education or buy a property are generally regarded as good debt, because both tend to deliver a return on investment.

However, you might not realise that taking on HECS-HELP debt can make it harder to qualify for a home loan and reduce your borrowing capacity. That’s because, if hundreds of dollars per month are being diverted from your salary to repay your student debt, that means you have less money to devote to mortgage repayments. So does that mean you should repay your HECS-HELP loan as soon as possible? Maybe yes, maybe no. On the one hand, eliminating your student debt could make it easier to get a home loan. On the other hand, student debt is interest-free (although it does increase in line with inflation), so it might be better to repay other interest-incurring loans first. Give me a call if you want to know the best approach for your situation or your child’s situation.  Buying a typical house will now cost you almost 30% more than buying the typical unit. CoreLogic has reported that, at the end of February, Australia's median house price was 29.8% higher than its median unit price – a record gap.  To put it in dollar terms, median prices are $791,400 for houses and $609,800 for units, which means the gap is almost $182,000.

That gap has significantly widened in the past two years:

On the other hand, it’s also possible the gap will narrow, because with houses looking relatively dear and units relatively cheap, demand might shift from the former to the latter.  The official data confirms what you might’ve heard anecdotally – property investors are very active right now. Property investors took out $33.7 billion of home loans in January, according to the Australian Bureau of Statistics, marking the second consecutive month in which investors set a borrowing record.  To illustrate how investment activity has surged in recent times, investors borrowed 67.8% more in January than the year before.

This increase has occurred throughout the country, with investment activity increasing by:

That means most property investors are finding it easy to secure quality tenants. It also gives many investors the chance to raise rents, because demand for rental accommodation is so high right now.  The supply chain shortages that have affected so many industries have hit property as well, with residential construction costs rising at the fastest annual rate since 2005.

Home building costs rose 7.3% in the 2021 calendar year, according to CoreLogic’s Cordell Construction Cost Index (CCCI). That said, the pace of growth might be trending down, with costs rising 3.8% in the September quarter but only 1.1% in the December quarter. Part of the reason costs are rising is because builders are struggling to get their hands on materials such as timber and metal products. Property developers and home builders are likely to be passing on at least some of these increased costs to people buying homes.  First home buyers can now save their deposit even faster, after the First Home Super Saver Scheme savings threshold was increased from $30,000 to $50,000.

The scheme lets first home buyers salary-sacrifice pre-tax income into a dedicated account within their superannuation fund – up to $15,000 per year and now up to $50,000 in total. There are two ways in which the First Home Super Saver Scheme benefits first home buyers. First, the money they deposit into the scheme is taxed at 15% rather than the income tax rate, which is 19% for someone earning up to $45,000 and 32.5% for up to $120,000. Second, when first home buyers eventually withdraw their money, they’re allowed to withdraw their original deposit plus about 4.7% interest, which is a higher rate of interest than they’d earn through a regular savings account. Withdrawals are generally taxed at the marginal tax rate minus 30 percentage points. |

AuthorRachael Bland – Founder & CEO Archives

February 2024

Categories

All

|

RSS Feed

RSS Feed

|

Privacy | Credit Guide | FAQs | Calculators

T: 0421 73 88 30 | E: rachael@getsmartfinancial.net.au Credit Representative Number: 427013 | Australian Credit Licence Number: 391237 | MFAA Accredited Credit Advisor 150638 | Copyright © 2019 Get Smart Results Pty Ltd |

Website by Mint Creative Circle

|